Capital Stack

As a long-time real estate practitioner, I’ve learned a few things over the years. If I can help just one person by sharing ideas and lessons learned, then this format will be worthwhile. Some have resulted from the joy of success, while others were learned the hard way. I promise to be transparent and not hold back. Sharing is how I choose to start my week.

June 1, 2026

Capital Stack

I have had several readers ask me, “What is a Capital Stack?” Well, in simple terms, it is a collection of participants playing different roles in a financial transaction. At a basic level, the capital stack is composed of two parts – debt and equity. Here is where it can get tricky.

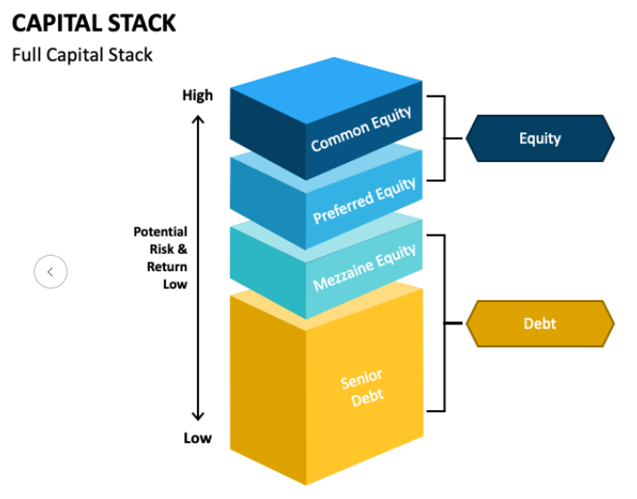

Each of these two parts can be further divided into multiple layers with different risks, returns, and preferential repayment treatments. Debt is the bottom portion of the capital stack and is sometimes referred to as “senior debt.” It takes on the highest priority for loan repayment by creating a “first lien” position on the investment. It is typically provided by a bank or other financial institution, which may be a government-sponsored agency (HUD, FNMA, FHLMC), a life insurance company, or a private equity (PE) firm. Being in first position for loan repayment carries less risk and less return as a result. The compensation for making these loans is limited to an interest return without sharing any upside or profits in the venture. There are also safeguards in place as to the maximum amount of the debt placed on a project. This is usually shown in terms of loan to value (LTV) or loan to cost (LTC).

If a low amount of senior debt is placed on a project a second layer of debt may need to be added. This is known as mezzanine or “subordinated” debt and bridges the gap between the senior debt and equity. It is subordinate to senior debt but senior to equity. As a result, it is riskier than senior debt and less risky than the equity portion of the capital stack. Lenders providing mezzanine debt receive returns through a combination of interest and equity participation.

The top of the capital stack is comprised of equity investment. At the conclusion of a project the equity shareholders are paid after the debt holders. Due to being in a riskier position, the projected returns for equity shareholders are higher as they divide the profit for the investment. There are multiple ways to split the profits within the equity portion of the capital stack.

If you read my article “Syndications and Deal Structure” recently you will remember the deal structure spells out the terms of the financial arrangements between the equity parties. Equity shares can be further divided into Preferred and Common shares or treated as a combination.

Like bondholders, preferred shareholders are entitled to regular, fixed dividends. They must be paid before any dividends are distributed to common shareholders. Dividends for common

equity are never guaranteed and paid out of profitability. Common equity shares offer unlimited potential for capital appreciation and are dependent on the success of the project.

Here’s a diagram of a typical capital stack highlighting potential risk and returns:

If you have questions about Capital Stacks or Deal Structures for Founders Development Company investments, please reach out for a consultation.